I am a confessed Early Retirement Enthusiast & I have blogged about my approach to retirement through Early Financial Independence. Saving & Investing for retirement is a good endeavor, something that most folks get serious about in their 40s in preparation for their golden retirement years into their 60s. However, the Early Retirement Enthusiast gets started much earlier, and typically takes on larger risk during the accumulation phase of their careers to amass the necessary corpus to enable financial independence at a much younger age. There is a strong emotional aspect to this journey, and I typically don't blog about my thoughts and feelings on that front. Here is an attempt at sharing with you how the emotional roller coaster ride feels like, as I approach financial independence.

I am a confessed Early Retirement Enthusiast & I have blogged about my approach to retirement through Early Financial Independence. Saving & Investing for retirement is a good endeavor, something that most folks get serious about in their 40s in preparation for their golden retirement years into their 60s. However, the Early Retirement Enthusiast gets started much earlier, and typically takes on larger risk during the accumulation phase of their careers to amass the necessary corpus to enable financial independence at a much younger age. There is a strong emotional aspect to this journey, and I typically don't blog about my thoughts and feelings on that front. Here is an attempt at sharing with you how the emotional roller coaster ride feels like, as I approach financial independence.

My 50+ year Retirement Roadmap describes the amount of corpus I need to have saved up to achieve my financial independence goal. Since I am targeting an earlier retirement, I needed to build additional margin of safety which is why you see my total corpus requirement exceeding 40X annual expenses. Bench-marking your retirement corpus in terms of your annual expenses is an excellent way to both plan for, and track your progress on this journey. In fact there is a school of thought that considers degrees of wealth as best defined in terms of annual expense multiples. I wrote a post about it yesterday called Uncle Scrooge and Donald Duck. You can figure out your target multiple by looking at this simple table I put together in this post titled How Much Should I Save before I Retire?

Today my networth is at 36X of my current annual expenses. This would likely be sufficient for a regular retirement, but is probably a little bit short for a comfortable 50+ year retirement plan. But that is a discussion for another post. For this one, let me focus on the journey building this 36X corpus.

0-5X: We first started on this quest, with a simple goal to put together a networth equaling 5X of our annual expenses. The idea was to start with a small but tangible goal that we could put all of our energies to. We were a DINK couple (Dual Income No Kids) in those days with no major expenses, and no EMIs. We have always chosen to live within the means of one income, which allowed us to sock away the second income as 100% investments. We have also been equity market addicts from the minute we had our own disposable income to work with, so we followed an all out equity investment strategy. We only did Mutual Fund investments in those days with no direct stocks exposure. There were no Direct MFs at that time, so we channeled all our MF investments through the ICICI-Direct portal. SIPs formed the bulk of our "financial planning". We chose SIPs not because we were trying to maximize returns, or achieve dollar cost averaging, or buy more units during market down swings, or anything like that. We simply did it because it was convenient. SIP it and forget it. Also as salaried employees it was the most natural way to invest, given the way our monthly salary based cash flows worked. Occasionally we would invest lump-sums into our favorite fund HDFC PRUDENCE MF, simply because it was one of the few well known available options at the time. We simply looked up options on Value Research Online, and invested through ICICI-Direct. No fancy calculators to review and recommend funds, just follow common-sense and invest. We did buy our TERM Insurance policies during this phase, though later in life we had to buy more insurance, since our coverage was very low initially.

We didn't do annual portfolio reviews or audits, there was no question of portfolio re-balancing since we were 100% in equity, and there was no concept of asset allocation since we only focused on equities. We didn't even do PPF allocations at this stage. Most importantly I think, we didn't follow any personal finance forums or discussions :-) which helped reduce the clutter in our thought process. It took us 5 years to achieve this objective, primarily fueled by our high savings rate since we kept one persons income solely for investments. Portfolio investment returns and growth were not a big factor since our overall portfolio size was small.

5X-10X: Encouraged by our initial success in putting together a 5X portfolio, we next launched into the 10X goal. We thought this would be relatively simple since all we had to do was double our already assembled corpus. Unfortunately this period coincided with the brutal fall in the markets in 2008. Instead of our corpus growing we actually were losing money at a rapid rate. The 100% equity exposure meant that our portfolio pretty much mirrored the 50% plus fall in the index. The only silver lining was that we didn't have any ultra aggressive small cap, or sector oriented funds in our portfolio, so our losses were not worse than the index. The good news is that since we were net buyers of equity, once the market recovered, in 2009-2010 timeframe, we actually came out ahead since our SIPs had continued right through the downturn. In fact we had invested more aggressively as the markets tanked with whatever spare funds we could lay our hands on. We still shunned direct equity, and focused on the MF route for all our investments. You can see the first half of the period I am referring to in the post Six Sideways Years. It took us 3 years to hit this goal. We had hoped that our initially saved corpus of 5X would grow and help us achieve this target. This did NOT happen. The 5X corpus barely recovered to its original size, but didn't really grow in this period. It was our SIPs during this time that benefited from the market downturn to amass wealth as the market finally recovered. We were fortunate that our salary incomes continued to rise during this time, like I discussed in Am I Earning Enough? We kept the discipline of maintaining our lifestyle at the same levels and investing any salary surpluses as quickly as we could into the market. Portfolio tracking continued to be sporadic, and no significant attempt was made to analyze our portfolio returns, asset allocation, MF selection, MF overlaps, volatility, short-long term returns etc. Additional TERM insurance was purchased since we realized we were not covered sufficiently

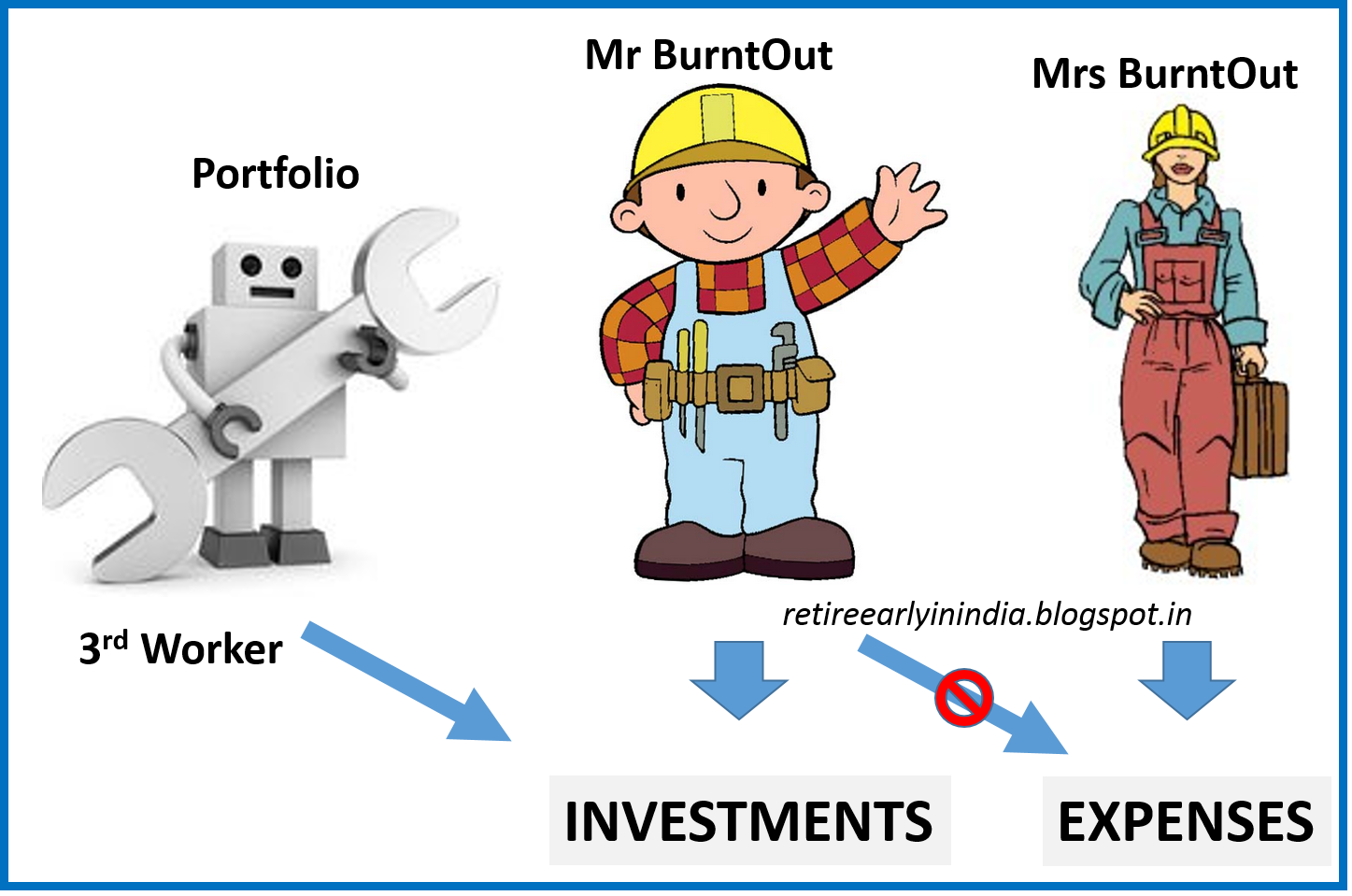

10X-36X: Our next target was to get to 20X, but we overshot that one, and managed to reach 36X in a mad dash based on the recent furious rally in the stock markets. Here our strategy of all out equity investments paid handsome dividends. I discussed this period of rapid growth and its impact on my portfolio in 6X Networth in 6 Years. Given that we were starting with a reasonable sized corpus of 10X annual expenses, we attempted in this phase to be a little more disciplined about our investing. We diversified our asset allocation a little bit, by getting into debt investments like tax free bonds and PPF. My EPF had also grown in this phase to a reasonable size. We also got adventurous and went into direct equity. I have shared my current asset allocation in the post A4 Portfolio. During this phase, we had the luxury of a 3rd contributor to our investment pattern.

Our investment portfolio had grown to a level wherein its growth contributions were now matching our own savings based contributions to the overall portfolio. The compounding effect of investing was finally kicking in, at a level where it could compete with us in our contributions to our retirement corpus. If you assume a 20X corpus, it takes a 5% increase in the stock market to push it up to 21X. This is the best representation of actual passive investment growth. Our efforts in adding to our retirement portfolio are currently dwarfed by the ability of the portfolio to grow. In effect it is like having one more earning member in the family. Except that this earning member never stops working, never takes a holiday, and is as productive if not more sometimes than we are. Yes we do have to provide guidance in the form of asset allocation decisions, MF selection etc, but we don't need to micro-manage him. My portfolio takes my high level guidance, and goes off and does its thing to deliver returns. Of course, the pinch comes during market downturns when Mr. Portfolio does a lousy job as well. But that is a discussion for another day! We continue to keep abreast of the latest developments in terms of market advances/declines, hot sectors, IPOs, NFOs, ULIPs, MIPs and what not. However, we rarely make any changes more than once per month. SIPs continue to run in auto-pilot mode. Direct equity is regularly looked at, but we rarely trade more than couple times a month. (We hold large cap stocks that have low volatility)

So in summary our first phase from 0-5X was characterized by ignorance, a rather cavalier attitude, but fortunately a sound investment strategy. 5X-10X started with despair, but also an obstinate drive to stay the course with equity investments, with our savings continuing to do most of the heavy lift. 10X-36X has reaped the benefits of a strong bull run on our earlier investments with our portfolio starting to outmatch our own contributions to the overall growth.

I have a fresh set of concerns as we go about topping off our retirement portfolio to add safety margin. These are primarily around protecting the corpus built up so far. I hope you found this write-up interesting, and would love to hear about your experience in building up your assets.

The content on this blog is meant to be aspirational and informative, written in an interesting yet quirky manner. If you like the writing style consider following this blog with your email address in the top right corner of this page. You will get an instant update notification for every new article that I post.

Hey,

ReplyDeleteI am really inspired after reading your articles. I am planning to quit my corporate job within next 10 years. I have been aggressively investing in mid cap equity funds to boost my returns. My current expenses stands out around 30K per month. Just like yours, I want to ensure my corpus supports me for 50 years post retirement. Post retirement my source of income would be from going for dividends option in equity funds, doing SWP,. The excess profits booked would be kept in PPF since the same would get mature in next 12 yrs. The added advantage being the ability to withdraw 60% of tax free corpus from PPF once we extend PPF subscription for block of 5 years.

I also wish to add real estate in my portfolio, to generate rental income and to make my portfolio diverse. However being a big ticket investment, I would have to delay buying it.

Thank you Smart Investor. Good luck in your quest for early financial independence, and let us keep sharing notes as we go along this journey. We can use all the encouragement we can get! Real estate provides inflation indexed returns, but the return percentage can be a low 2-3%. I have discussed my post retirement asset allocation plan here in this post http://retireearlyinindia.blogspot.in/2015/07/my-50-year-retirement-map-do-i-even.html It is important in my opinion to keep a baseline portion of your post-retirement portfolio in debt instruments, and invest only the excess in equity. I intend to keep 10 years worth of expenses in pure debt funds

ReplyDeleteHey,

DeleteI completely agree with you that one should have debt component in one's portfolio and for that my PPF account and having FD's in name of adult child should suffice to generate tax free and assured returns.

Real estate is something which can diversify my portfolio and generating decent passive income. However going for real estate, would require me to liquidate all my current assets

Hi,

ReplyDeleteI came across your blog only yesterday and was very impressed and you do have lot of very interesting articles. I work in IT industry and have been very focused on achieving financial independence and I am very close to it as my target was to be financially free at 40 and planning to retire from active job and do what I Love/Like in next few months. I would like to share my plan with you privately and obtain your feedback, pls do let me know your private email id.

regards,

satish

my email id is satish.vs@gmail.com

ReplyDeleteThis comment has been removed by the author.

ReplyDeleteHi,

ReplyDeleteI would like to read your points regarding protecting your corpus. In my case I am forced into early retirement at 46 with 2 small kids with around 45x savings I would like to protect it for nect 20 years to release funds for my daughter and son education and marriage also I would like you to include tax planning on income generated by corpus as it will be taxable thanks